Background

From competitive gap to competitive edge

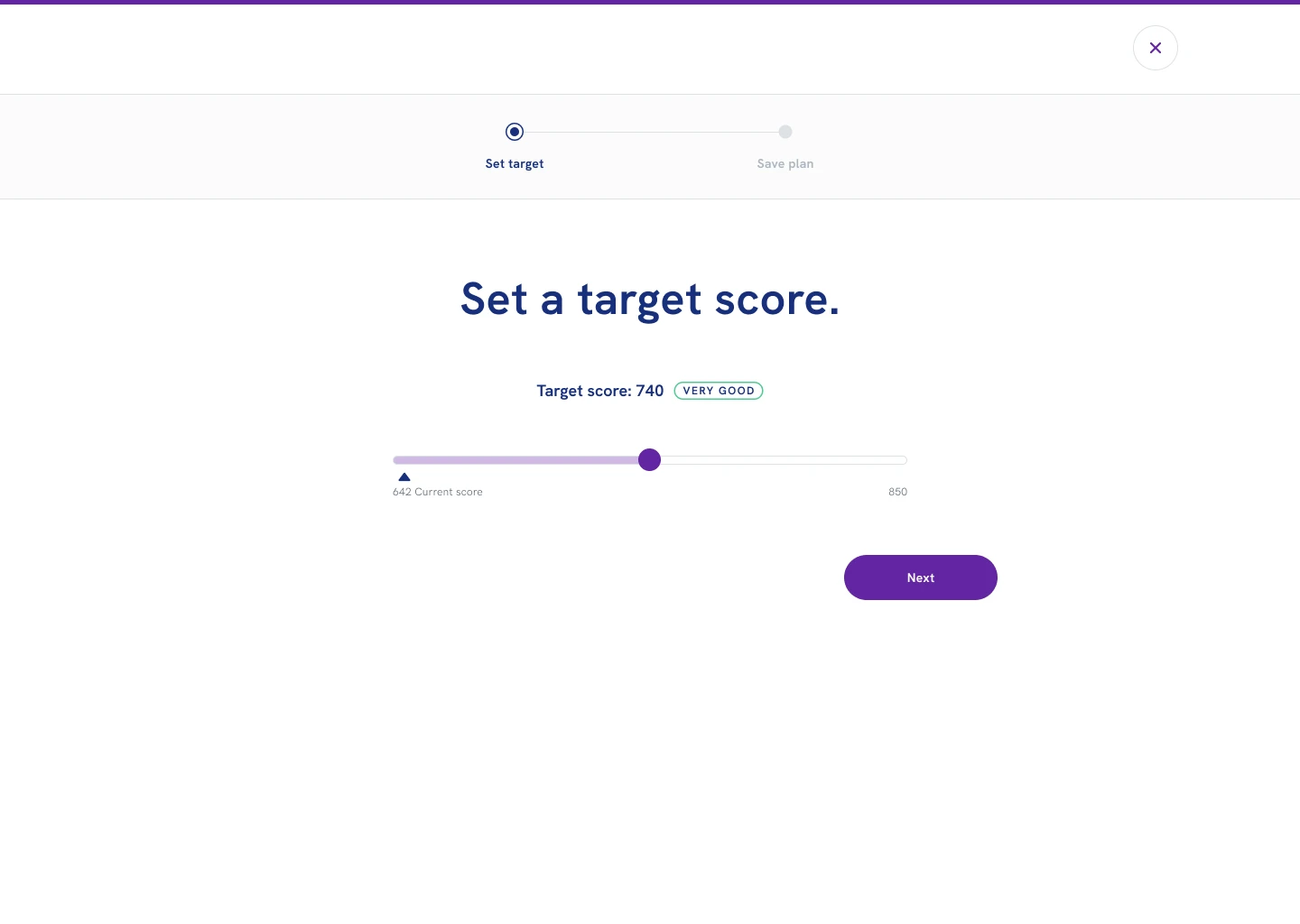

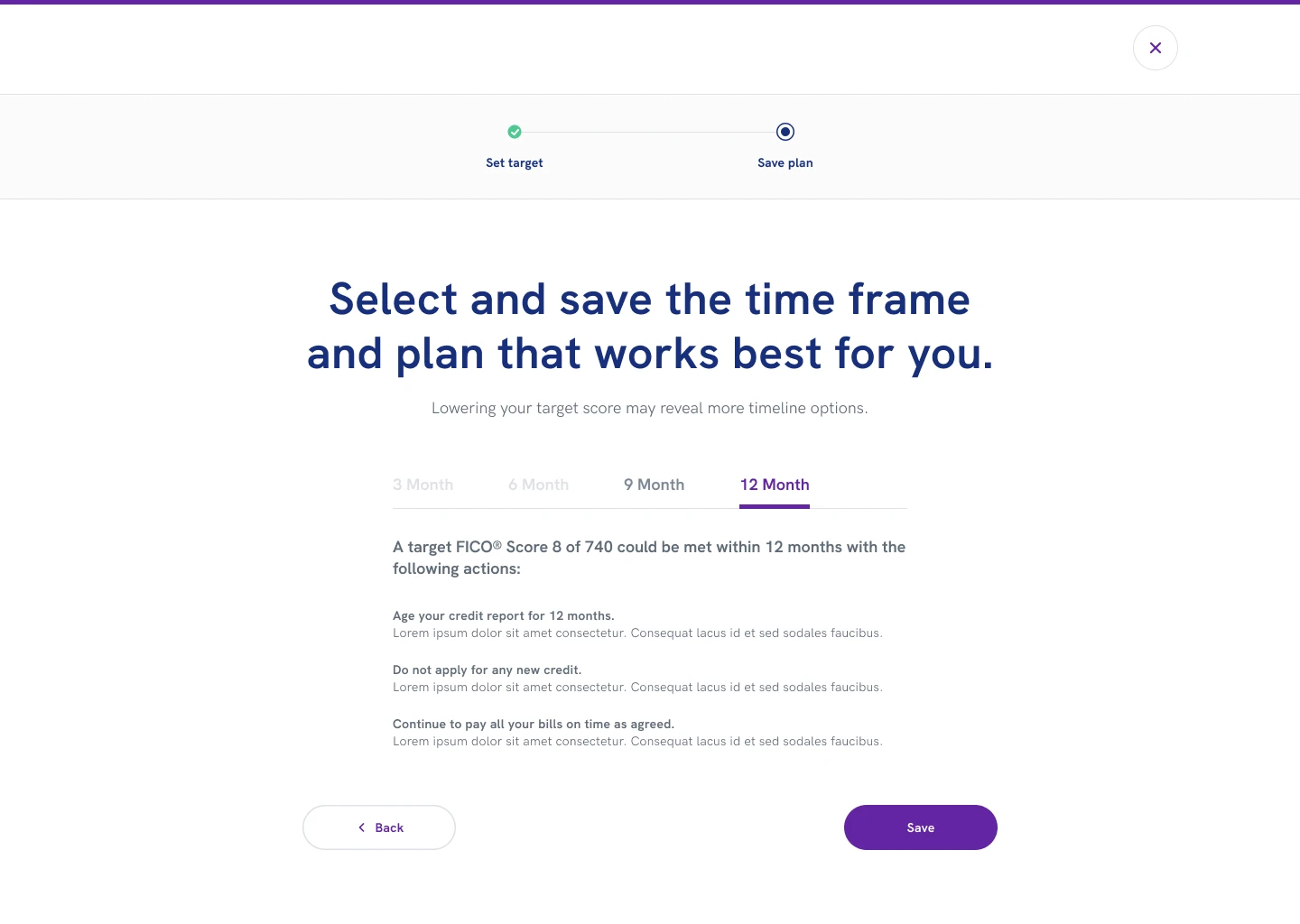

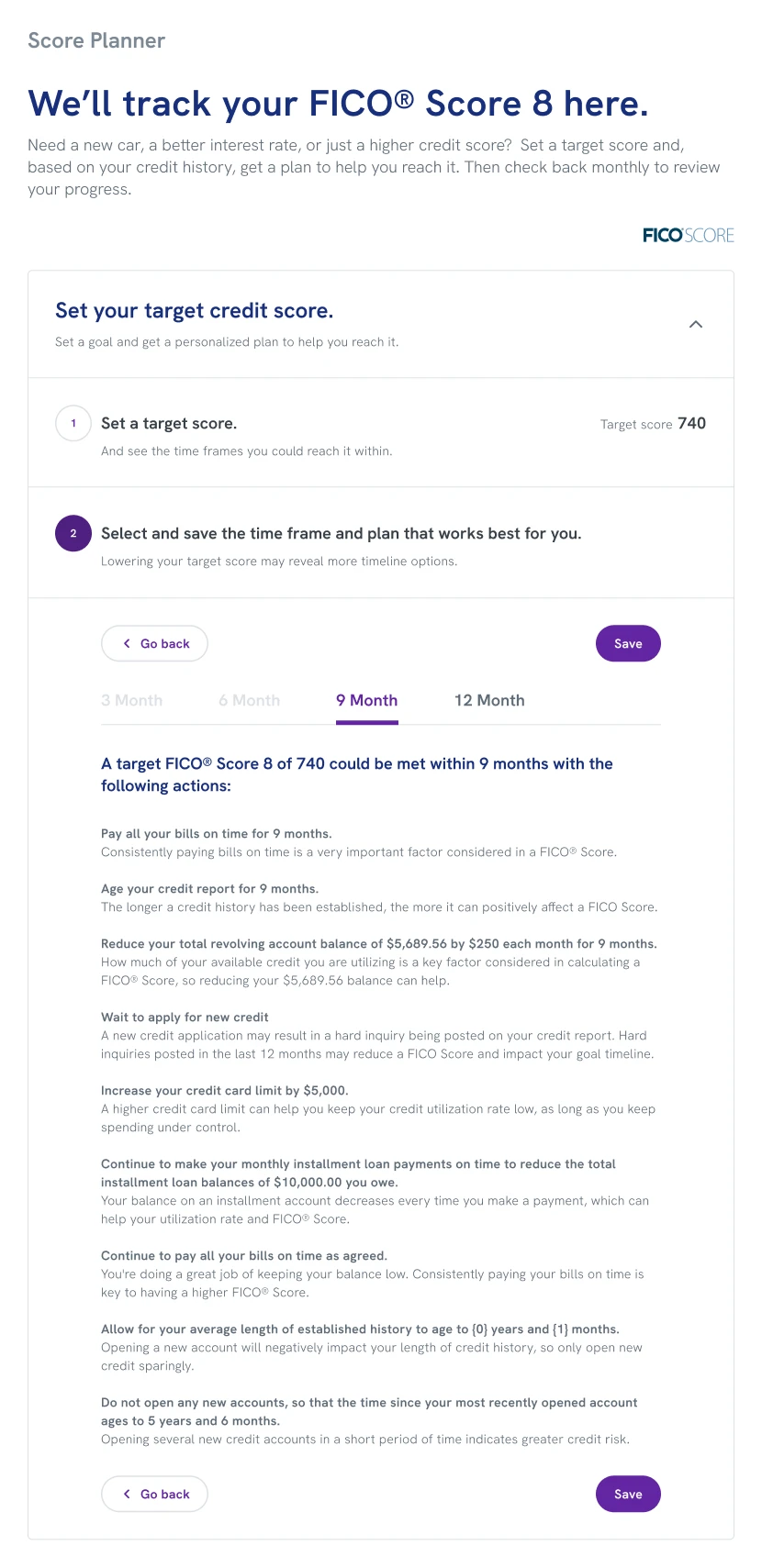

Experian Partner Solutions provides a platform of financial wellness tools that partners brand and offer directly to their users. A Score Planner lets users set a target FICO Score, understand what actions could help them reach it, and track their progress over time — turning an abstract number into a goal with a path.

The gap was two-layered: a key competitor offered a Score Planner, but only for VantageScore. A marquee partner wanted FICO — and we had nothing to offer. Building it would close the deal and fill a genuine product gap across the entire EPS partner network.

Competitor 1

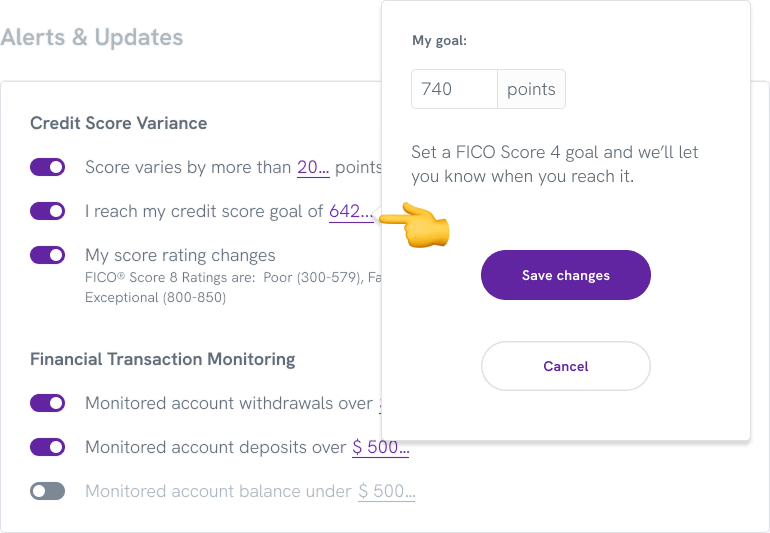

The red target is draggable, but there is no indication of the restrictions: the target score must be at least 10 points higher than the current score, and not all timeframes are available for every target.

Competitor 2

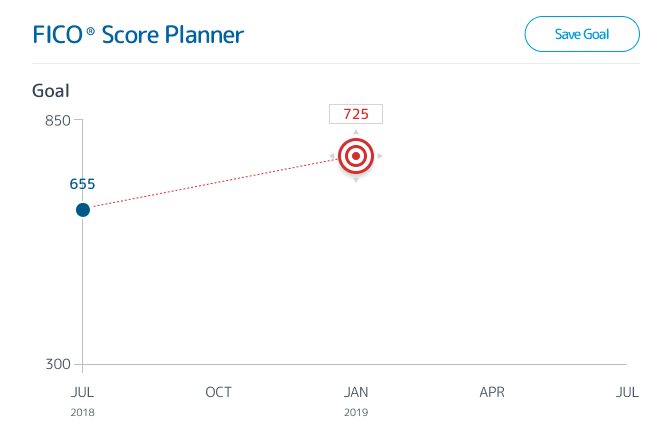

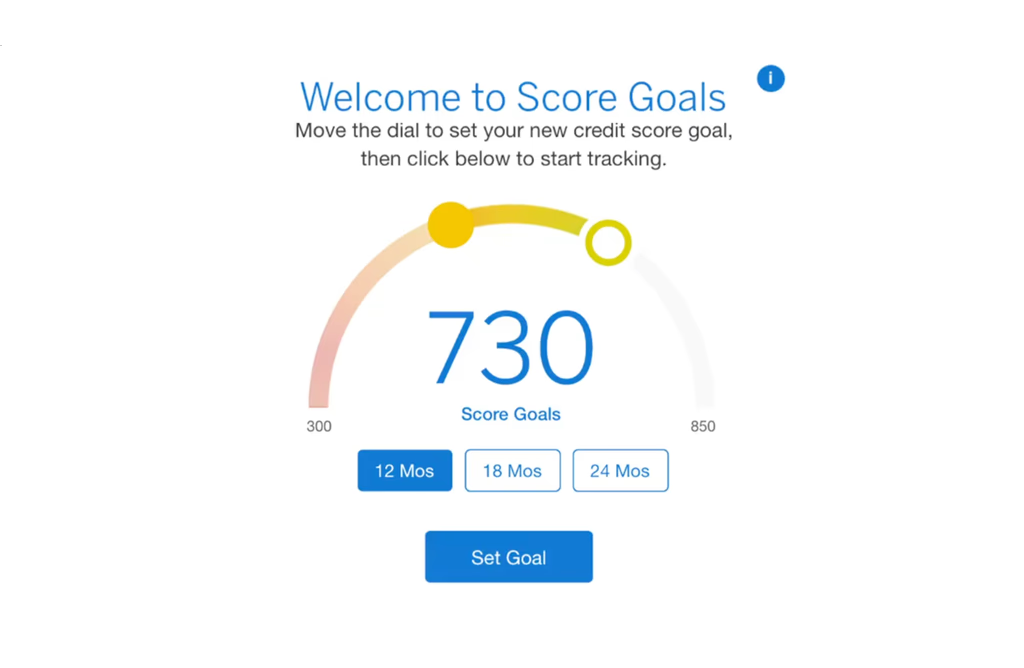

The user selects a timeframe, then uses the slider arc to set the score goal, and clicks to set it. Once a goal is set, the steps needed to achieve it are revealed.